Selecting the incorrect repayment strategy could lead to significant financial losses or extend your debt repayment period by years. This is not an exaggeration; it highlights the stark differences between IBR and RAP. Some borrowers may find IBR more advantageous, while others might benefit from the reduced monthly payments under RAP. Unfortunately, no one will decide for you which plan suits you best. This guide aims to assist in making that choice.

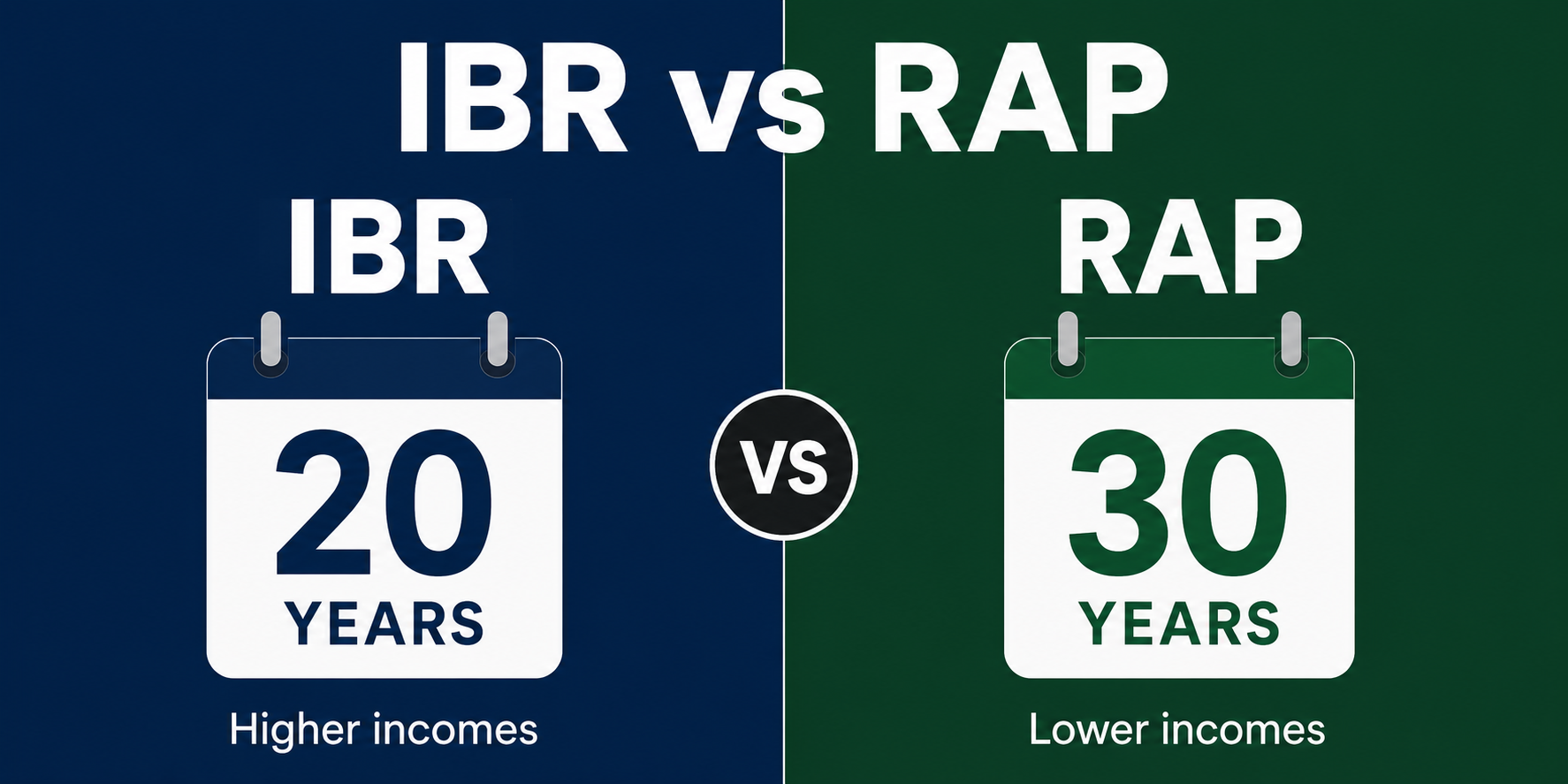

For those earning a high income, typically over $80,000, IBR is often the better option. Borrowers with low to moderate income, usually under $80,000, might find RAP more beneficial. If you’re nearing the forgiveness period of 20 or 25 years, IBR might be preferable. Those concerned about their balance increasing due to interest should consider RAP. When pursuing PSLF, choose the plan with the lower monthly payment. After July 1, 2026, RAP becomes the primary IDR option for new borrowers. In cases where one partner earns significantly more, IBR might be advantageous, but calculations are necessary. Families with dependent children may find RAP competitive due to a $50 deduction per child.

Income-Based Repayment (IBR) has been available since 2009, linking payments to income rather than loan balance and offering forgiveness after 20 or 25 years. There are two versions: Old IBR, for those with existing federal loans as of July 1, 2014, charges 15% of discretionary income with forgiveness after 25 years. New IBR, for borrowers after July 1, 2014, charges 10% with forgiveness after 20 years, offering lower payment rates. Both versions cap payments at the standard 10-year plan level, and very low incomes could mean $0 payments. For new federal loans taken after July 1, 2026, IBR won’t be available, shifting borrowers to RAP or the Tiered Standard Plan.

The Repayment Assistance Plan (RAP) launches on July 1, 2026, following the One Big Beautiful Bill Act of 2025. RAP is the sole income-driven option for new borrowers after this date, while IBR remains for those with prior eligible loans. RAP calculates payments as a flat percentage of adjusted gross income (AGI), scaling with income. A minimum payment of $10/month applies, and the government subsidizes any unpaid interest. Forgiveness occurs after 30 years. RAP’s Matching Principal Payment provision ensures meaningful principal reductions each month, even if payments are modest.

IBR and RAP calculate payments differently. IBR uses discretionary income, subtracting 150% of the federal poverty line from AGI. For example, a $50,000 income results in payments on $26,000. RAP directly charges a sliding percentage of total AGI without a poverty-line buffer, offering a $50 deduction per dependent child. RAP often results in lower payments at lower incomes, while IBR is advantageous at higher incomes due to the poverty-line buffer. Calculations should consider income growth over time, as RAP’s scaling rate might shift the cost balance.

Analyzing three borrower profiles: A single borrower with a $40,000 income pays approximately $138/month under IBR for 20 years versus $100/month under RAP for 30 years. The savings come at the cost of a longer term. A single borrower with an $85,000 income pays $513/month under IBR, $54 less than RAP, with faster forgiveness. For a borrower with two kids earning $55,000, IBR’s $125/month payment slightly beats RAP’s $129/month, but RAP’s interest subsidy could sway the choice if balance growth is a concern. These estimates use 2026 federal poverty guidelines.

Original Source: studentloansherpa.com