On March 31, 2026, the Department of Education revised the calculation method for PSLF Buyback amounts for borrowers under the SAVE plan. The new calculations will use IBR, PAYE, or ICR formulas, which are more costly. For instance, under the SAVE formula, a borrower might owe $4,300, but with IBR, this could rise to $12,800. Those with pending buyback applications may face higher amounts than anticipated.

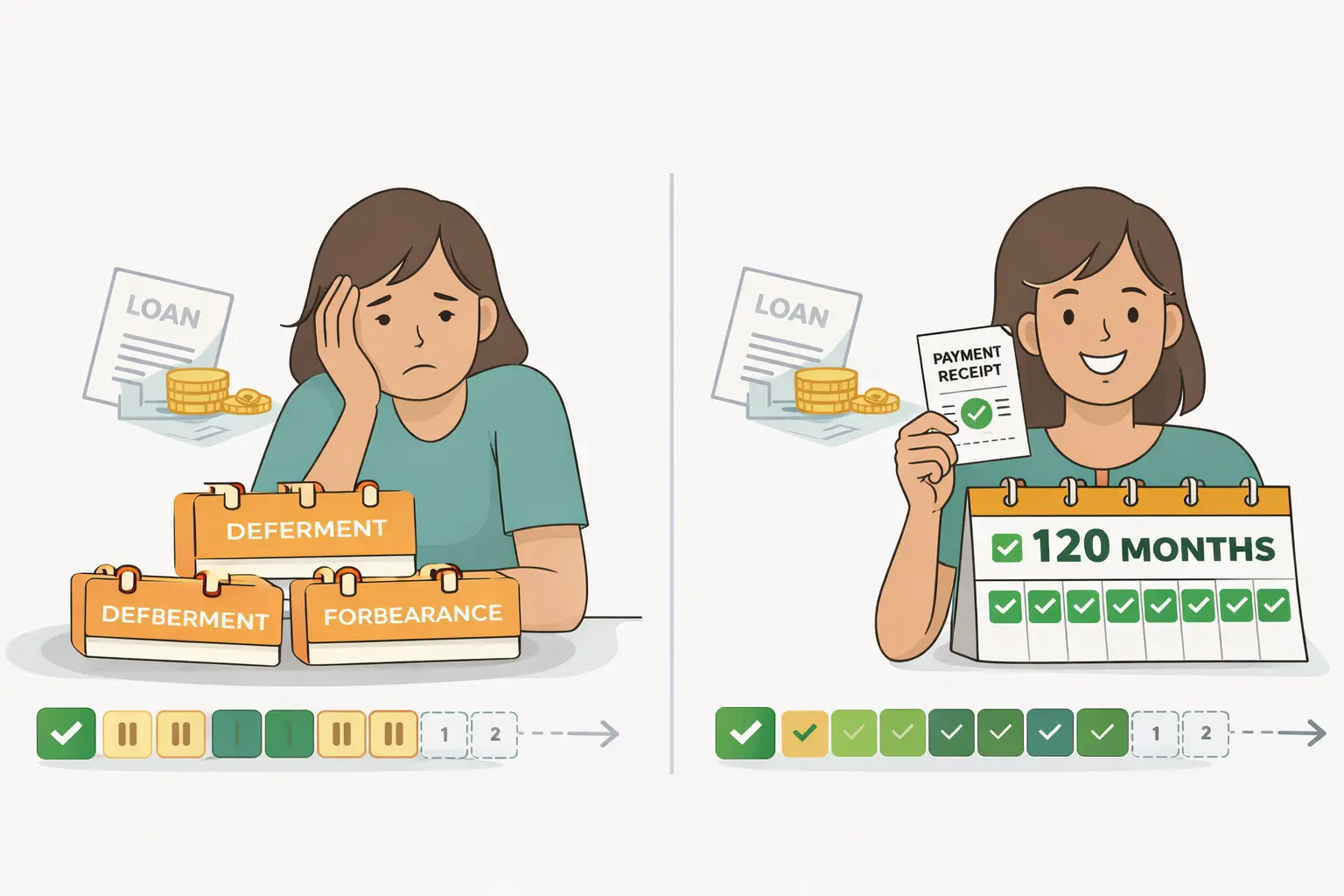

PSLF Buyback allows borrowers to convert deferment or forbearance months into qualifying PSLF payments by making a lump-sum payment equivalent to their income-driven payment for those months. This can help borrowers nearing forgiveness, who may find that certain deferment or forbearance periods do not count towards their 120 required payments. The guide provides detailed instructions on applying for and understanding PSLF Buyback in 2026.

PSLF Buyback benefits borrowers with 120 months of certified qualifying employment but lacking the same number of qualifying payments due to deferment or forbearance, such as during the COVID-19 payment pause. It is available for those needing immediate forgiveness, but only if the additional months achieve this. Borrowers from the SAVE payment pause must convert those months to qualify, once they reach 120 qualifying employment months.

PSLF forgiveness is always tax-free at the federal level. For many, the buyback can be financially advantageous; for example, buying back eight months of forbearance with a $75 IDR payment costs $600, leading to full loan forgiveness. However, buyback is only sensible if it directly results in forgiveness. Borrowers not close to 120 payments should continue paying and revisit buyback later.

To be eligible for PSLF Buyback, one must have a Direct Loan with an outstanding balance, sufficient certified qualifying employment, and deferment/forbearance months with qualifying employment. Loans already paid off, forgiven, or discharged, and months before a consolidation loan’s first disbursement are ineligible.

By September 2024, consolidation uses a weighted average of qualifying payment counts. If considering PSLF Buyback, review payment history before consolidating, as months prior to the first disbursement of a consolidation loan are not eligible. From July 1, 2026, consolidating loans eliminates access to legacy IDR plans, leaving only the Repayment Assistance Plan, which may increase monthly payments.

COVID-19 forbearance months already count as $0 qualifying payments if employment is certified. Buyback should be considered if these months are marked ineligible. Eligible deferments and forbearances include the COVID-19 payment pause, financial hardship, medical or dental residencies, military duty, and more. Ineligible statuses are in-school deferment, grace periods, default, bankruptcy, and disability monitoring periods.

Borrowers should track deferment and forbearance months diligently to prepare for when buyback becomes available, ensuring they can maximize their path to loan forgiveness.

Original Source: studentloansherpa.com